In today’s seller’s market, it’s not out of the ordinary to receive more than one offer on a listing. In fact, these days it’s more like the norm. According to the July 2021 NAR REALTORS® Confidence Index (RCI) survey, the average number of offers received on a home is more than 4.

As a listing agent, receiving multiple offers on your property is a dream scenario. You’ve done your job as an agent, and your seller now has multiple options to choose from—some better than they could have ever imagined. But the work doesn’t stop there. The offers may be in, but your client still needs your guidance.

It’s your duty to help guide your seller to choose the best offer for them, and that means presenting the offers in a way that makes sense to your seller. This task isn’t all that difficult when you have only one or two offers on the table. But when the offers start rolling in and you’re faced with presenting four plus offers to your client, this task can easily become overwhelming.

So, what do you do? How do you ensure you’re providing the best guidance to your seller? The short answer: you need a system.

Whether you’re about to list a property or already have multiple offers on the table, we’ll explore what’s needed to ensure you have everything in order to best support your client in their decision.

But first, a quick note about ethics

Not only do you have a duty to your client, you also have an obligation to treat all offers—and buyers—fairly. According to NAR’s Code of Ethics & Standards of Practice, that means every offer must be presented to your client. The only exception being if your seller waived the obligation and communicated in writing that they do not want to see an offer if it doesn't meet certain criteria. For instance, if the offer comes in below a certain price (i.e. I don’t want to see offers less than $400,000).

Alright, now that we’ve cleared that up, let’s see how we can make your job easier by developing a tried-and-true system for presenting and comparing offers.

Understand your client’s needs and priorities

Before you even start to receive offers, talk to your client about what’s most important to them when it comes to the sale of their home. Hopefully, you’ve already had this conversation when you were hired to list their home, but if you haven’t or are unclear on the details, now is the time to get crystal clear on what they want.

Does your client want to maximize their return? Is flexibility important to them? Ask them what their priorities are for selling. Having this knowledge will allow you to communicate their preferences to interested buyer’s agents and help you get more competitive offers for your client.

Insider Tip: When you use Jointly to manage offers on your listings, you can make this process even easier by including your seller’s preferences on your listing’s offer portal. Buyer’s agents will be able to review terms that are important to your client, and in turn, craft a more compelling offer. Keep reading to find out how Jointly can help you collect, receive, and compare offers!

A well-informed agent means a client who is better equipped to make the decision that’s best for them. In the end, helping your client navigate multiple offers becomes easier when you thoroughly understand their needs.

Implement a system for receiving offers

What system do you have in place for collecting offers? Do you have a system at all? Let’s explore the different options you have at your disposal starting with the most common—email.

The status quo system

Today, most agents receive offers through email. Although the most common, email certainly isn’t the best option for the job. When you have dozens of offers coming in within a matter of days—potentially on multiple properties—any semblance of order goes out the door. When your inbox is cluttered with offers, there’s no order, just chaos.

Instead, you need a dedicated system, or more accurately, a portal for receiving offer submissions. Generally speaking, a portal is a centralized place where buyer’s agents can submit their offer to you.

A good system

There are plenty of tools out there that can be used to accomplish this. One of the simplest ways is to create a digital form for buyer’s agents to submit their offers.

You can use a forms tool like Google forms, Jotform, or Typeform. Then, create a form with the fields needed to get a high-level view of the offer (more on what fields should be included below). When you’re ready to start receiving offers, drop the link into the MLS private remarks instructing agents to submit their offers via the form. Submissions would then be collected in your software of choice, typically a spreadsheet.

The form system is a simple solution to get your “portal” up and running, but this option also comes with a few downsides:

Extra work for the buyer’s agent

After buyer’s agents have already drafted their offer, you’re asking them to re-enter information about their offer in yet another form. They’ll likely go ahead and submit the form if they have their client's best interest in mind, but you may get some pushback.

Inconsistent results

Because you’re leaving it up to the buyer’s agents to input information, what they enter may not be standardized (i.e. one agent may enter the down payment as a percentage and another as a dollar amount), resulting in more reformatting work for you later on.

Prone to error

The chance for human error also increases and may result in discrepancies between what’s actually in the contract and what’s on the form.

Extra work for you

Even if the information flows into a spreadsheet, you’ll probably have to do quite a bit of additional work to get it into a digestible format that your client will understand.

Similarly, most offer management solutions on the market today are just this. They don’t integrate with state and local forms, lack electronic signature, and are prone to more work rather than less work—contributing to a greater possibility of human error and inaccuracies. Fortunately, there’s an even better system that addresses and eliminates these pitfalls.

A better system

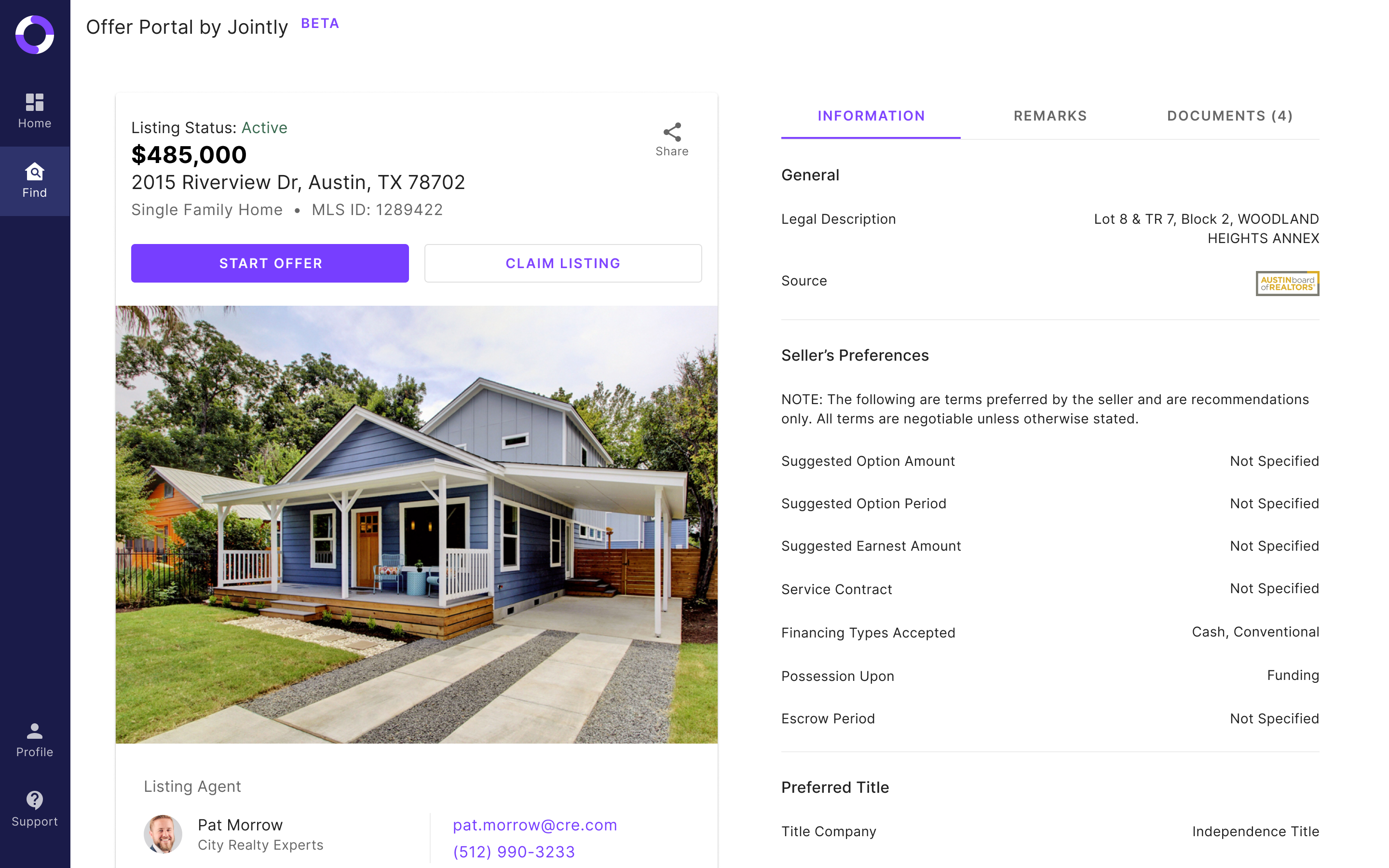

An offer management system, like Jointly, is a far better option for receiving offers. With Jointly, every listing has its own dedicated offer portal where agents can see information about the property and seller preferences, as well as submit offers.

One of the major differences between Jointly and the other options is that Jointly allows buyer’s agents to write, sign, and submit offers on the platform for free. There’s no need for them to draft their offer and then re-enter key terms on another form.

Instead, when an offer is submitted through Jointly, all offers are automatically added to a centralized offer inbox where the listing agent can view key terms, download documents, and compare offers side-by-side. It’s a win-win.

Decide how you’ll present offers to clients

Now that you have a system in place for receiving offers, next you’ll want to determine the best way to present them to your client. Let’s explore a few options along with their pros and cons.

3 methods for presenting offers to clients:

1. Spreadsheet. Likely the most common choice among listing agents is presenting offers via spreadsheet.

- Pro: Spreadsheets are great for calculating and organizing numeric data which makes them an obvious choice for displaying quantitative offer terms.

- Con: However, spreadsheets aren't always easy to digest. You’ll likely need to do a little extra formatting to make it easier for your clients to understand.

Need some inspiration for your offer comparison spreadsheet? Download our free offer comparison template here.

2. Slide presentation. If you’re looking to give your offer comparisons a bit more polish, slide presentations may be the way to go.

- Pro: Slide presentations provide an easy way to present information without overwhelming your client. Each offer can be broken down on each slide. Presentations also allow you to add more polish and design.

- Con: It can be difficult to compare offers and terms side-by-side, especially since you only have so much real estate to work with on one slide.

3. Offer comparison tool. Offer comparison tools come in different shapes and sizes, but typically incorporate both the benefits of spreadsheets and slide presentations into one solution (pssst..we recently released our own offer comparison tool as part of the Jointly platform! Sign up to try it for free).

- Pro: Offer comparison tools automate the comparison process, extracting information from the contract and presenting it in a clear and digestible format that requires no extra work from the agent. Tools like Jointly give you the added flexibility to choose which terms and offers to compare with just a few clicks.

- Con: Offer comparison software may not be free to use.

Once you know what method you want to use to present offers, it’s time to determine exactly what type of offer information should be included.

Determine which terms to include in your offer comparison

There are over 50 fields in a typical single-family home contract. While each of these fields is needed to complete the contract, not every single one needs to (or should) be included in an offer comparison.

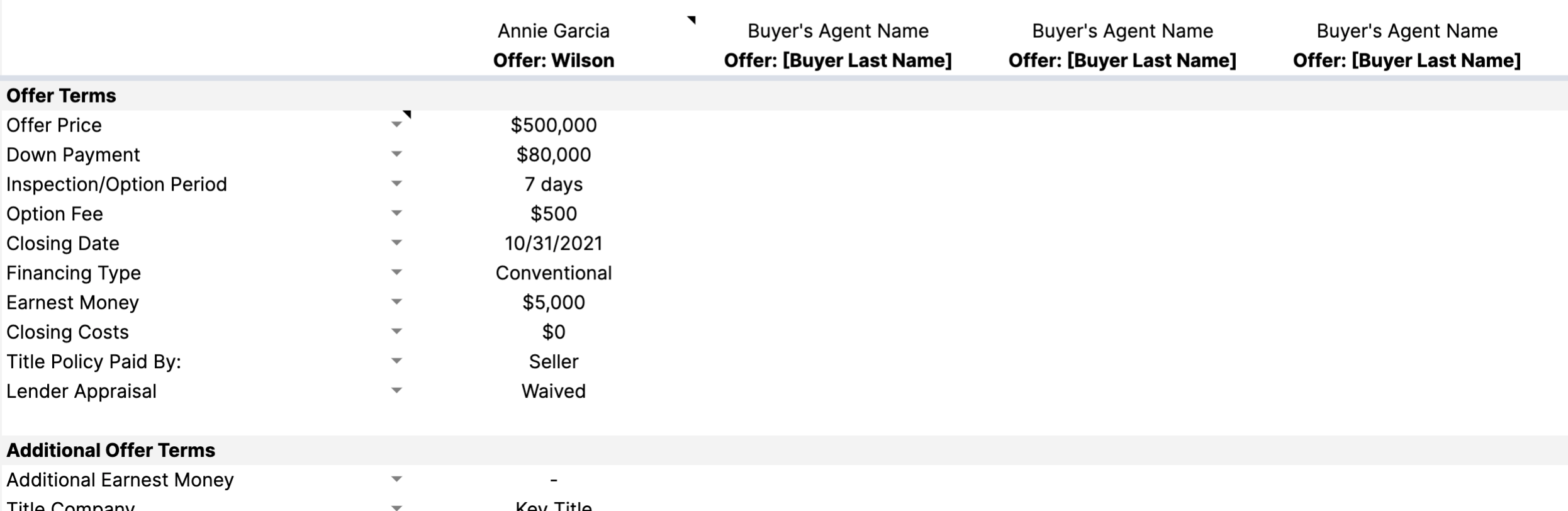

When creating an offer comparison sheet, first, start with the information needed to correctly identify each offer. This should include the:

- Agent’s name

- Buyer’s last name

Next, list out the basic terms of the offer. At a minimum, this should encompass the:

- Offer price

- Down payment amount

- Inspection (or option) period

- Option fee (if applicable)

- Closing date

- Financing type

- Earnest money deposit

- Buyer closing costs paid by the seller

- Who pays for the title policy

- Lender appraisal waiver (if applicable)

Other terms you might want to include:

- Financing amount

- Additional earnest money

- Escrow

- Financing approval

- Home warranty amount

- Max interest rate

- Owner’s title policy amount

- Who purchases a new survey (if applicable)

Once you have those basic terms, add a section to denote any special conditions associated with each offer. This may include things like:

- Home sale contingency

- Non-realty items (and the cost of those items)

- Seller leaseback

Download this offer comparison template for free ->

In the end, the comparison sheet should include all the pertinent details that you need to present the offers to your client in a clear and concise way. But a great agent takes this a step further, helping their client to see the big picture. Afterall, a home warranty of $500 to be paid by the seller might not mean much to them without any context.

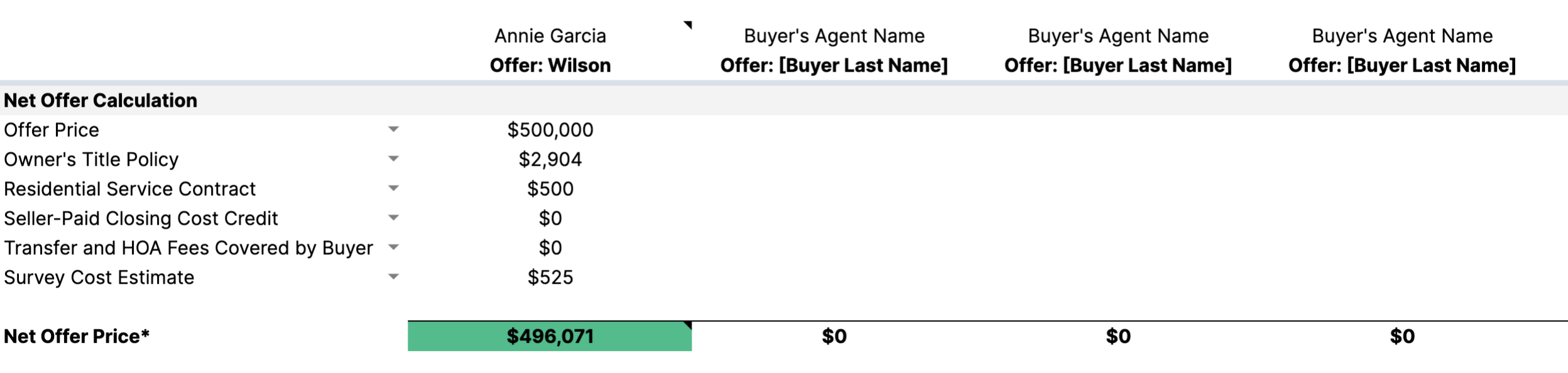

Calculate the net offer price

In order to help your client not only see the offers they’ve received, but really understand how each term impacts them, you need to show them the bottom line. Ultimately, what are they going to get from the sale if they choose one offer over another?

The net offer price helps your client compare offers apples to apples. To calculate the net offer price, subtract any offer term that impacts the overall offer price, including terms like:

- Owner’s title policy amount

- Home warranty contribution

- Any buyer’s closing costs paid by the seller

- HOA transfer fees

- New survey costs

If any of these terms require the seller to pay a certain amount, then these amounts should be deducted from the offer price. By doing this, your client will be able to see the true value of each offer and make the decision that’s best for them.

Need a template for calculating net offer price? Download our free offer comparison spreadsheet ->

How is net offer price different from net proceeds?

Net proceeds are the profit your client makes from the sale of their home. The net proceeds are calculated by subtracting the costs of selling (which includes agent commission and other closing fees) and the loan payoff from the sales price of the home.

Unlike net proceeds, net offer price doesn’t take into account all the costs of selling, but only the offer terms that affect the overall offer price. When comparing offers, you should only include terms that are specific to each offer. After your seller has accepted an offer, then it’s good practice to prepare a full net proceeds sheet for your client.

At the end of the day, it’s your client’s decision, but it’s your responsibility to represent and counsel them the best way you can. By following the steps above, you’ll ensure you’re fully meeting your obligation to your client and helping them navigate multiple offers with confidence and ease.